Independent swiss private bank founded in 1982

o the point

Independent swiss private bank founded in 1982

Banque Thaler is a boutique private bank exclusively dedicated to wealth management for private clients. We do not engage in investment banking, nor do we extend commercial loans or mortgages. We focus on selected areas of business but strive to do them well.

Banque Thaler is ‘Switzerland only’-based, with offices in Geneva and Zurich. The Swiss virtues of stability, quality, precision and craftsmanship are deeply ingrained in how we operate and serve our clients.

Banque Thaler is independent and owned by a partnership of management and board members. The owners thus manage the business and are directly involved in looking after our clients – with a long-term perspective. We are free from external pressures and our interests are aligned with those of our clients. Indeed, our first and foremost focus is on our clients, aiming to be their trusted advisor.

Banque Thaler has an entrepreneurial spirit and a lean organisation. Our human size translates into robust decision-making, high reactivity and flawless execution. The services that we offer are personalised and can be delivered in several European languages.

At Banque Thaler, we view dynamic asset allocation as key to generating positive investment returns. To build client portfolios, we apply a top-down approach. Allocation decisions, between cash, bonds, equities and alternative funds, are taken by the Investment Committee, based on a thorough fundamental analysis of the global macro-economic environment – with a focus on longer run trends mainly, rather than short-term market noise.

We have a longstanding tradition of investing in hedge funds. Over the years, we have developed a high level of expertise in selecting these complex products and built a network of trusted partners, making for sustainable results in all market circumstances. Our clients thus have access to the most experienced managers, whom we submit to an extensive due diligence process.

Should you want to fully rely on our expertise, skills and constant focus on financial markets, you may consider granting us a discretionary mandate. This means letting us make the investment decisions on your behalf, based of course on your financial needs, long-term objectives, risk appetite and country of domicile. Using a dynamic approach, we optimise portfolio diversification through best-in-class investment solutions. The goal being both to preserve your capital and to outperform the relevant benchmarks.

An advisory relationship involves combining our respective expertise and know-how of financial markets and instruments. When you have investment ideas, we act as your sparring partner. And we provide proactive and customised advice, in line with your appetite for risk. Knowing that the final investment decision always remains yours.

24 April 2024

Banque Thaler is very happy to be a partner of this great event organized by BDFil Lausanne. Because Comic Strips are an Art. Incredible what a drawing can bring to communication, convey a message, an atmosphere, a synthesized thought, an

15 April 2024

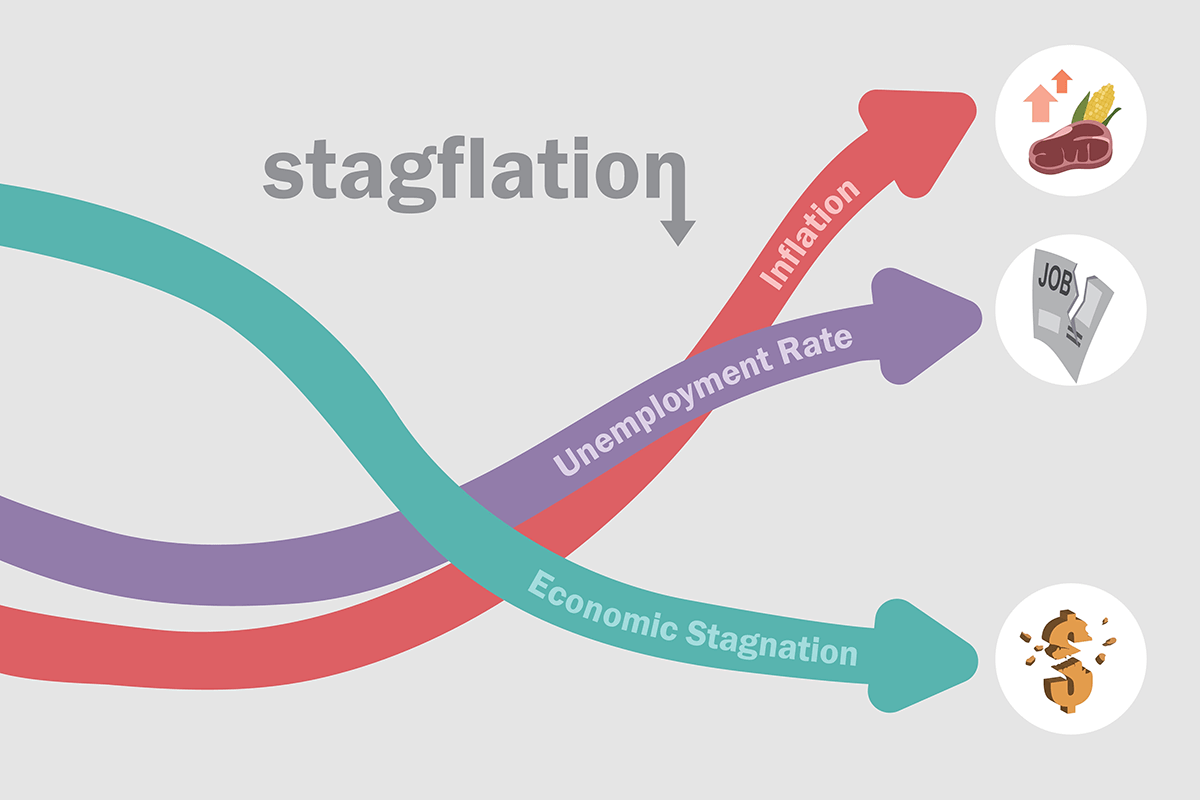

Just when the major financial actors had lowered and postponed their rate cut expectations, better aligning them with Federal Reserve and European Central Bank projections, the Swiss National Bank surprised everyone by cutting its policy rate by 0.25% on 21

15 March 2024

Fitting together the pieces of today’s economic and financial puzzle is no easy task. What is the true state of the Chinese economy? How will the geopolitical situation evolve in the Middle East and Ukraine? What will the US presidential

12 February 2024

Recent data reports continue to point to a solid economy and receding inflation, particularly in the US. So much so that the US central bank, while acknowledging that monetary policy will indeed be pivoted this year, has advised markets to

15 January 2024

Equity markets were in good spirits during the final weeks of 2023, buoyed by receding inflation expectations – hence hopes for rapid rate cuts. Increased geopolitical concerns were blithely ignored in the process. But what are the odds of the

11 December 2023

Geopolitical developments took somewhat of a backseat during November and, with inflation continuing to move down amid still resilient US activity, bond and – especially – equity markets have been in a festive mood. The odds of an economic soft

10 November 2023

Geopolitics unfortunately took centre stage again in October, with a brutal conflict erupting in the Middle East. The overall economic picture, meanwhile, continues to deteriorate as the effects of 18 months of monetary tightening begin to take their toll. Yet,

16 October 2023

The major take-away of the past few weeks has been the breakout in long-term yields. The 30-year US Treasury briefly hit 5% in the opening days of October, certainly an important threshold for investors. And a similar move is underway

15 September 2023

Contrary to common assertions, we do not consider the situation on the energy front to be that rosy. Oil is once again trading around USD 90 per barrel, meaning that its past months’ moderating effect on overall inflation indices has

10 August 2023

On Wall Street, July saw a continuation of the strong June market performance, with the large technology names again posting the largest gains. To the point that Nasdaq decided to trim the weightings of the “Magnificent Seven” components of the

JEAN-YVES DE BOTH

Chairman of the Board

GREGOIRE WUEST

Boardmember

STEFAN SABLON

Boardmember

HERMAN WIELFAERT

Boardmember

DIRK EELBODE

CEO

OLLIVIER GUERIN

COO

CHRISTIAN MOREL

CFO / CRO

PASCAL BLACKBURNE, CFA

CIO

NADINE MERTENS, MSc

Private Banker / Associate Partner

ANTON EIKHOUT, LL.M.

Head of Zurich Office / Associate Partner

SABINE NEYMAN, MSc

Private Banker / Associate Partner

DIDIER DE TERWANGNE

Private Banker / Associate Partner

EDMONDA PELEMAN

Private Banker

HANNEKE VAN DER MEER, MA

Private Banker

INGE KUPFER SESSA

Private Banking

SONIA CROZET

Secrétariat / Réception

TITA SAGARMINAGA

Private Banker

OLIVIER MULIN

Portfolio Management

STEFAN OLDENZIEL, LL.M.

Private Banking / Associate Partner

NATHALIE PALMEN

Private Banking

JEAN-LUC MONCALVO

Trade Execution

GASPAR MOTTE

Private Banker

LIVIA HERRIJGERS, CFA

Head of Portfolio Management

BEN SABBE, CFA

Portfolio Management

ROXANE PIETTE

Private Banking

CÉCILIA JACQUÉRIOZ

Deputy CIO

COLETTE LE RAY

Private Banker

VANESSA RACLOZ

Private Banker

RAYMOND VAN WIJNEN

Private banker

PIETER DE BISSCHOP

Private Banking / Director

PEGGY CORNELISZ

Private Banking

We would be glad to welcome you in one of our offices in Geneva or Zurich.

Rue Pierre-Fatio 3, CH-1204 Genève

Kämbelgasse 6, CH-8001 Zürich